Commissioner v. Tufts

United States Supreme Court

461 U.S. 300 (1983)

- Written by Sara Rhee, JD

Facts

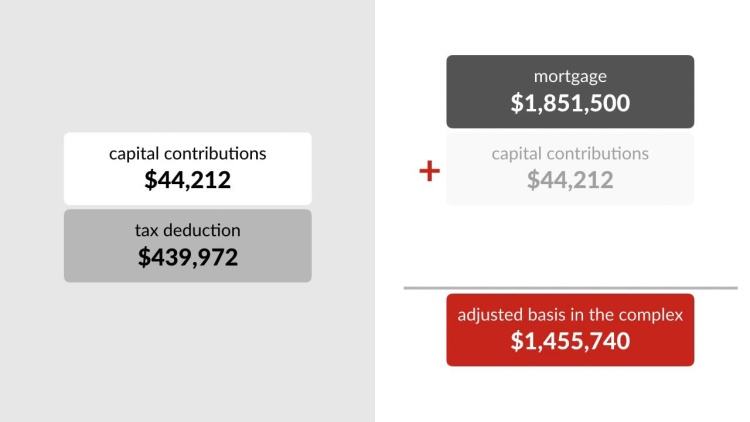

A general partnership (plaintiffs) formed to build an apartment complex. The partnership obtained a nonrecourse mortgage on the building in the amount of $1,851,500, and the partners made capital contributions in the amount of $44,212. For the next two years, each partner took depreciation deductions totaling $439,972. In light of their capital contributions and depreciation deductions, their adjusted basis in the property in 1972 was $1,455,740. But due to economic problems in the area, the partnership was unable to pay the mortgage, which still had a balance of approximately $1,850,000. Each partner sold his share to a third party, who assumed the nonrecourse mortgage. A dispute arose regarding the complex's sale value for tax purposes. The partners calculated the sale value as the property's fair market value, which was about $1,400,000. Because the property's market value was less than the property's adjusted basis, each partner reported a loss of $55,740 from the sale. However, the Commissioner of the Internal Revenue Service (defendant) calculated the property's sale value as the $1,850,000 balance of the transferred mortgage. Because the mortgage balance was higher than the property's adjusted basis, and determined the partnership had realized a capital gain of about $400,000. The tax court agreed with the commissioner. The court of appeals reversed. The United States Supreme Court granted certiorari.

Rule of Law

Issue

Holding and Reasoning (Blackmun, J.)

Concurrence (O’Connor, J.)

What to do next…

Here's why 926,000 law students have relied on our case briefs:

- Written by law professors and practitioners, not other law students. 47,400 briefs, keyed to 1,003 casebooks. Top-notch customer support.

- The right amount of information, includes the facts, issues, rule of law, holding and reasoning, and any concurrences and dissents.

- Access in your classes, works on your mobile and tablet. Massive library of related video lessons and high quality multiple-choice questions.

- Easy to use, uniform format for every case brief. Written in plain English, not in legalese. Our briefs summarize and simplify; they don’t just repeat the court’s language.