Poe v. Seaborn

United States Supreme Court

282 U.S. 101 (1930)

- Written by Robert Taylor, JD

Facts

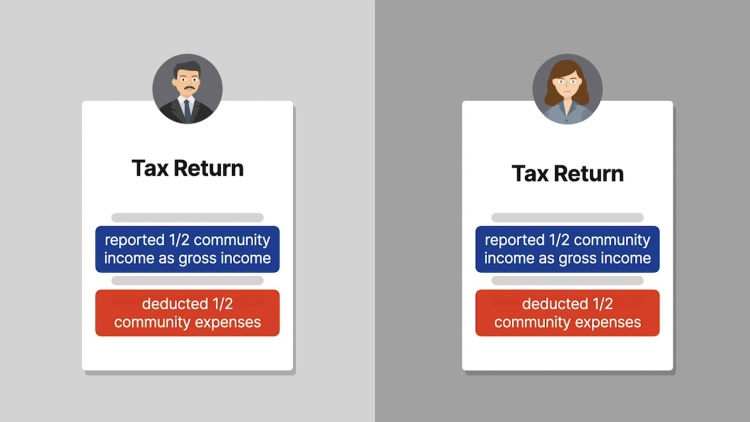

Mr. and Mrs. Seaborn (plaintiffs) resided in Washington, a community-property state, and filed separate federal income-tax returns. On their tax returns, the Seaborns each reported, as gross income, one-half of Mr. Seaborn’s salary and one-half of the proceeds from the sale of real estate held in Mr. Seaborn’s name. By dividing the income as opposed to filing jointly, the Seaborns were able to lower their tax bracket. The federal tax commissioner (commissioner) (defendant) issued a deficiency notice against Mr. Seaborn, determining that all of his salary should been reported as gross income on his own individual tax return, rather than divided with Mrs. Seaborn. The Seaborns filed suit against the commissioner in federal district court, seeking a tax refund. The district court entered judgment in favor of the Seaborns, holding that they were entitled to file separate tax returns with each claiming one-half of the community income. The commissioner appealed. The court of appeals certified the issue to the United States Supreme Court.

Rule of Law

Issue

Holding and Reasoning (Roberts, J.)

What to do next…

Here's why 928,000 law students have relied on our case briefs:

- Written by law professors and practitioners, not other law students. 47,400 briefs, keyed to 1,003 casebooks. Top-notch customer support.

- The right amount of information, includes the facts, issues, rule of law, holding and reasoning, and any concurrences and dissents.

- Access in your classes, works on your mobile and tablet. Massive library of related video lessons and high quality multiple-choice questions.

- Easy to use, uniform format for every case brief. Written in plain English, not in legalese. Our briefs summarize and simplify; they don’t just repeat the court’s language.