Taft v. Bowers

United States Supreme Court

278 U.S. 470 (1929)

- Written by Sara Rhee, JD

Facts

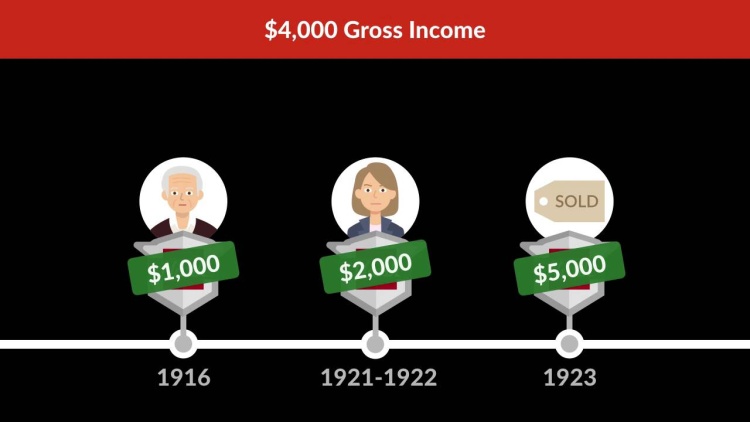

Elizabeth C. Taft (plaintiff) received 100 shares of stock from her father as a gift in 1921 and 1922. Taft’s father had purchased the shares in 1916 for $1,000. At the time of transfer, the shares of stock had appreciated to $2,000. In 1923, Taft sold the shares for $5,000. The United States calculated a $4,000 increase in income based on the $1,000 appreciation during the father’s ownership and the $3,000 appreciation during Taft’s ownership, and taxed Taft accordingly. Taft paid the tax but subsequently sued for a refund, arguing that only the $3,000 increase during her ownership was income, and that the Sixteenth Amendment prevented Congress from taxing her for any increase during her father’s ownership. The District Court held in Taft’s favor. The Court of Appeals reversed. The United States Supreme Court granted certiorari.

Rule of Law

Issue

Holding and Reasoning (McReynolds, J.)

What to do next…

Here's why 926,000 law students have relied on our case briefs:

- Written by law professors and practitioners, not other law students. 47,400 briefs, keyed to 1,003 casebooks. Top-notch customer support.

- The right amount of information, includes the facts, issues, rule of law, holding and reasoning, and any concurrences and dissents.

- Access in your classes, works on your mobile and tablet. Massive library of related video lessons and high quality multiple-choice questions.

- Easy to use, uniform format for every case brief. Written in plain English, not in legalese. Our briefs summarize and simplify; they don’t just repeat the court’s language.